A company’s ability to understand its financial position is an important part of its success. Financial reporting is one tool that can help you, to assess your company’s financial health which is an objective way. A financial statement, the product of financial reporting, can show if your company is profitable or headed for trouble. Let’s understand the basics of company QuickBooks financial statement.

What are Financial Statements?

Reports are known as financial statements that provide an explanation of the profitability and financial performance of an organization over a specific period of time. Balance sheets, income statements (sometimes known as profit and loss statements), and cash flow statements are the three fundamental types of financial statements. Less often, business owners use other financial reports like the statement of retained earnings.

Why QuickBooks Financial Statements are Important?

Financial statements are important because they provide information about a company’s overall financial performance and health to creditors, shareholders, and regulators. In an annual report, public companies are needed to publish their financial statements. Financial statements often include details regarding a company’s:

- Economic resources and obligations

- Earning capacity

- Potential cash flows

- Management status

- Accounting policies

Above all, financial statements give business owners a clearer understanding of their bottom lines and enable them to make more informed decisions.

How are QuickBooks Financial Statement Prepared?

Financial statements are essential sources of financial data, thus to guarantee accuracy and consistency, you must follow fundamental accounting standards. Three principles can be used to prepare financial statements, or you can use our free QuickBooks financial statement template.

1. Recorded facts

You can prepare financial statements with the help of an original or historical cost of accounts. Generally, you keep track of pricing and the original cost of assets you buy at different times.

2. Accounting conventions

Financial statements that follow accounting conventions are more realistic and comparable. For example, accountants must apply standards consistently year after year to applyith the principle of consistency.

3. Personal judgments

To avoid overstating assets and liabilities, your financial statements are dependent on estimates and personal judgments.

Now that you have understood the concept of financial statements, let’s check the many reports that make up financial statements.

3 Types of Financial Statement in QuickBooks?

There are various tools available to business owners in the financial reporting industry to help them complete tasks, but important tools that are typically included in the business owner utility belt:

Balance sheet:

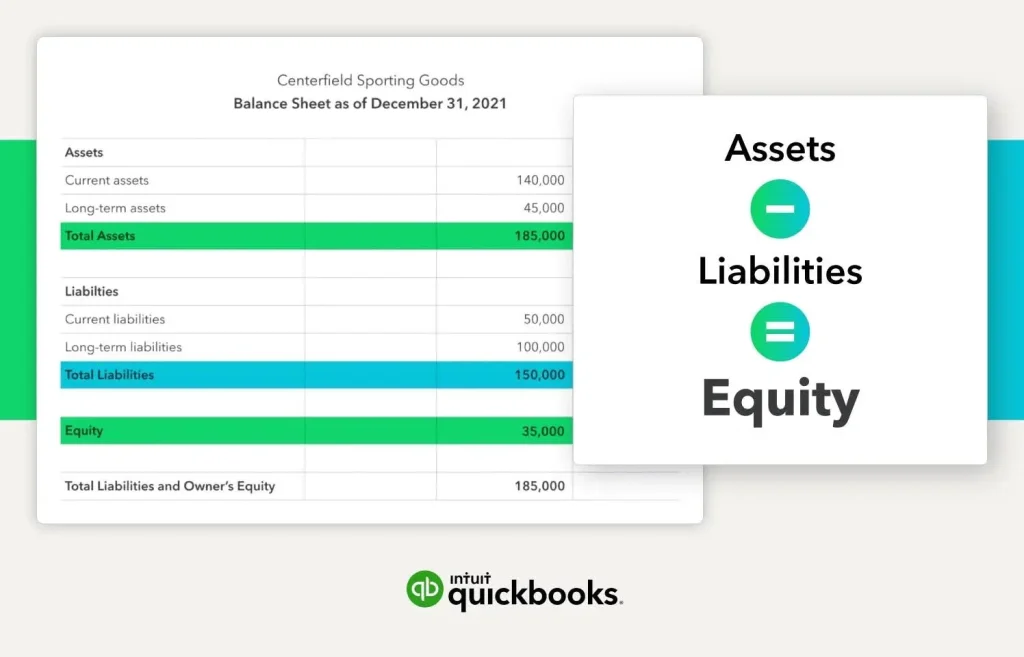

A financial statement that shows the balances of a company’s assets, liabilities, and equity is called a balance sheet, often known as a statement of financial condition. It will display the business’s financial position at a particular point in time. Three categories are listed on a balance sheet: assets, liabilities, and shareholders’ equity.

Assets: Resources that generate revenue (or sales) and profits for a company are called assets. An asset can be tangible, such as vehicle, or intangible, like a patent or other intellectual property. Current assets like accounts receivable are included in this.

Liabilities: Liabilities are the amount owed by the business to third parties, including both long-term debt and accounts payable (also known as current liabilities).

Equity: The true value of a business is represented by equity, which is the difference between its assets and liabilities. Retained earnings, additional paid-in share capital, and common inventory are all considered forms of equity. Equity can also refer to net worth, owner’s equity, or shareholder’s equity.

The three parts of the balance sheet are operated by the balance sheet formula. Liabilities are subtracted from assets in the formula to determine equity. The formula follows:

Assets – liabilities = equity

As transactions post the double-entry accounting system will need the accounting equation to stay in balance. Working capital and other important ratios are calculated using balance sheet accounts.

Review Centerfield Sporting Goods’ balance sheet as of December 31, 2021. otal assets ($185,000) equals the sum of total liabilities ($150,000) plus equity ($35,000).

How is a Balance Sheet Connected to an Income Statement?

The net income account connects as the link between an income statement and the balance sheet. The income statement formula can be used by a company to create its income statement. It calculates net income by subtracting expenses from revenue. The following is the formula:

Revenue – expenses = net income (net profit)

Because the account balances on income statement accounts reset to zero at the end of each month and year, they are sometimes referred to as temporary accounts. Accounts on a balance sheet, however, are permanent. From one month to the next the ending balance is carried.

The books close at the end of each month, and all expense and revenue accounts are adjusted to zero. The activity’s posts net impact on the income statement increases the equity balance and reflects as net income on the balance sheet.

Also Read: Process Credit Card Payments in QuickBooks Online

Income Statement

An income statement displays the revenue expenses for a specific time period for a company. It offers data on risks, operating capabilities, financial flexibility, and return on investment. An income statement is produced by the income statement formula. The majority of companies create a multi-step income statement that outlines the process by which they generate net income.

How Does a Multi-Step Income Statement Differ?

A multi-step income statement shows your operating income for a given period of time after your gross profit.

Let’s say you own a small furniture company and are preparing an income statement for May that involves several steps. Most of your business operations will revolve around gross profit.

Your overhead, labor, and material expenses are posted to the cost of products sold. You made $1,200,000 in furniture sales in May, bringing your total cost of goods sold (labor and material expenses) to $900,000. That means your gross profit was $300,000.

However, you also had to pay for home office expenses, commissions on sales, and advertising in May to run your company. Assume for the moment that the costs came to $170,000 each month. To determine your $130,000 operational income for May, deduct your $300,000 profit from your $170,000 expenses.

Operating income vs. non-operating income

Daily business activities might provide you with operating income. Operating income from furniture sales was $130,000 in May. In addition, your business brought in $4,000 from the equipment sale and $2,000 in interest income. Thus, your net income for May is $136,000 in total.

Because operating income is sustainable, most of your company’s net income must originate from these sources. Non-operating income needs to be more consistent and predictable. It is not a reliable source of yearly profits for any business.

Review the income statement for the Centerfield company for December 2021. $520,000 was sold, while $420,000 was spent on sales expenses. Their total profit was therefore $100,000. Additionally, Centerfield’s operational costs came to $90,000. As a result, their operational income for the time was $10,000. The company’s operating income was its net income balance because it did not generate any non-operating income.

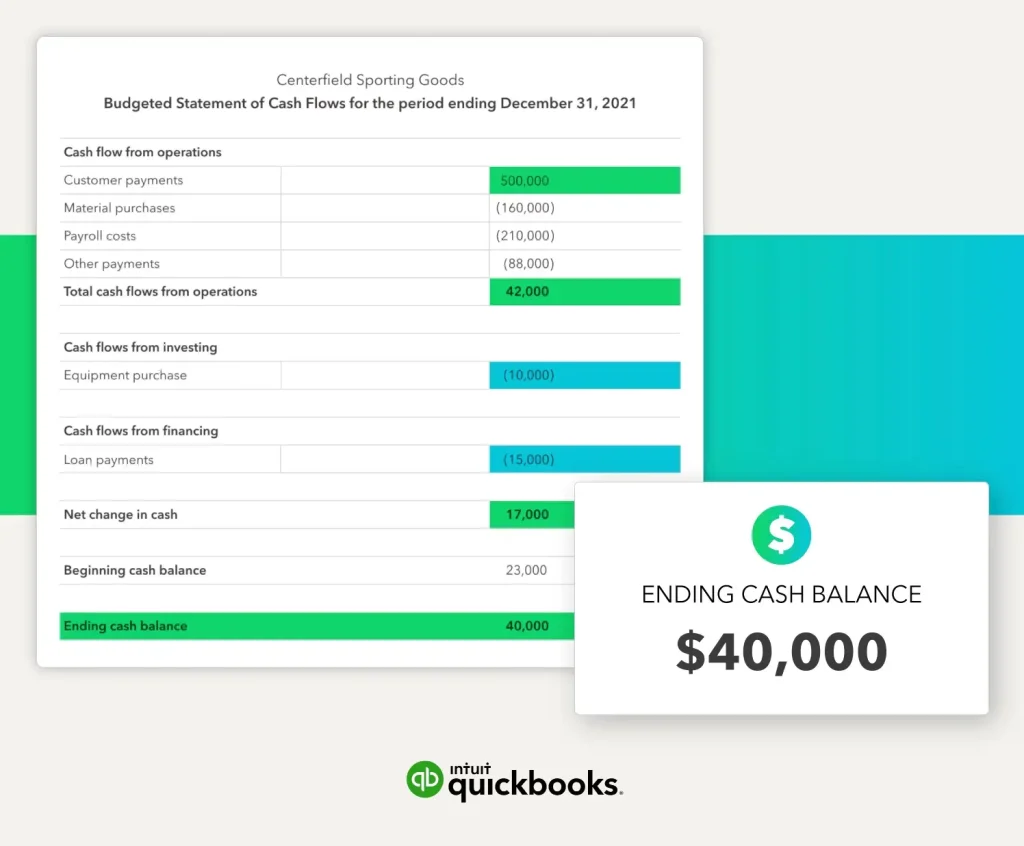

Cash Flow Statement

The cash inflows and outflows of a business are shown in the cash flow statement, also known as the statement of changes in financial position. Three categories exist for cash flow.

- The sources and uses of cash related to a business’s everyday activities are indicated by its operating activities. Inventory and cash from customer sales are examples of operating activities. The majority of a company’s cash flow should come from regular operations, which can continue for months or even years.

- Cash transactions involving the buying and selling of assets such as machinery, equipment, and cars are referred to as investing activities.

- When a business makes money through the issuance of bonds or stocks, financing activities take place. Repayment of cash to investors is also included in the category of financial activities.

The operating category of a business is where most of its cash activity occurs. An accountant should start by identifying the financing and investment transactions while creating the cash flow statement. The operating category includes all remaining monetary activities.

Examine Centerfield’s cash flow statement for the fiscal year that concluded on December 31, 2021. Keep in mind that the balance sheet’s cash amount ($40,000) and the ending cash balance are the same.

How a Statement of Cash Flow is Connected to the Balance Sheet?

To find the net change in cash for a given period, the statement of cash flows adds up all cash inflows and outflows. The balance at the end of the cash flow statement and the balance sheet should be the same.

Also Read: Create Invoice in QuickBooks Desktop & Online

Creating more Accurate QuickBooks Financial Statement

In the end, automating the process wherever it is practical can greatly improve the dependability and accuracy of your financial accounts. For example, using accounting software makes use of technology to manage all the number.

Thus, the days of sifting through piles of receipts and pressing buttons on the adding machine calculator are over.

Selecting and following the accounting rules is another strategy for maintaining accurate financial statements. When attempting to compare current performance to previous years and becoming disoriented by different accounting or categorization systems, it can be very difficult.

However, there are a few ways that financial statements might be inaaccurate or inefficient.

4 Common Mistakes in Financial Statements

An important component of any financial accounting system is a financial statement. Your financial accounts and company decisions may not be as accurate if you make one of these common mistakes.

- You are not including comparative data.

It is simpler to see whether actual numbers match expectations when prior-year, prior-month, or budgeted amounts are included

- You are not showing reality.

A company’s actual financial situation should always be reflected in its financial statements. To find errors, think about having a third party examine your financial statements.

- You’re not updating the process to lessen inconsistencies.

Take the time to update your accounting practices if you find an error or disparity in your financial statements.

- Your financial statements are not being audited.

Only when financial statements are correct can they be useful. Don’t create a financial statement merely for documentation’s sake. Study the statement, make any necessary corrections, and use it to gain a better understanding of the financial situation of your company.

Conclusion!!

Generating and analyzing QuickBooks financial statement is important for understanding your business’s financial health. Reports like the Balance Sheet, Profit and Loss Statement, and Cash Flow Statement provide insights into performance, inform business decisions, and aid in tax preparation. Regularly reviewing and customizing these reports helps track progress, identify trends, and correct discrepancies. Using QuickBooks’ robust reporting capabilities ensures greater financial clarity and control over your operations. For assistance or advanced financial analysis, our team is available round the clock.

Frequently Asked Questions (FAQs):

Q1. What financial statements can I generate in QuickBooks?

Ans. QuickBooks allows you to generate key financial statements such as the Balance Sheet, Profit and Loss Statement (Income Statement), and Cash Flow Statement.

Q2. How do I create a Profit and Loss Statement in QuickBooks?

Ans. To create a Profit and Loss Statement, go to the “Reports” menu, select “Company & Financial,” and then choose “Profit & Loss Standard.” Customize the report dates and other parameters as needed.

Q3. What information should be included in the Balance Sheet report?

Ans. The Balance Sheet report provides a snapshot of your company’s financial position, including assets, liabilities, and equity, as of a specific date.

Q4: Can I customize financial statements in QuickBooks?

Ans. QuickBooks allows you to customize financial statements by adjusting the date range, adding or removing columns, filtering data, and modifying the layout and style to meet your specific needs.